While still in its infancy, non-QM lending is expected to get a major boost in 2018, this according to a forecast from S&P Global Ratings.

The company said it expects the non-QM market to double or possibly triple in 2018 from current levels.

They point to a more liquid non-QM market, driven by improved and more efficient securitization, which should also lower spreads and make such lending cheaper.

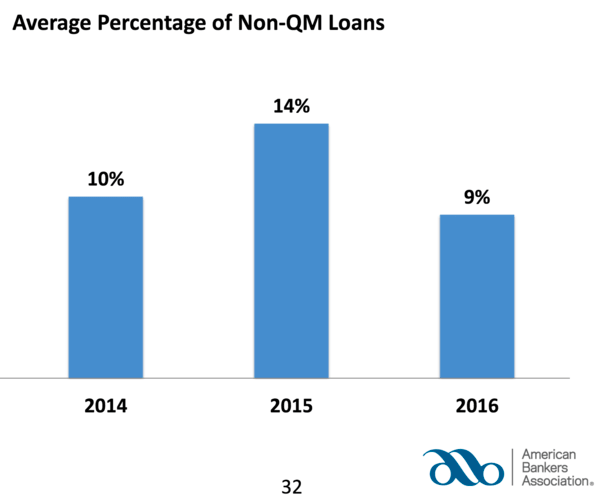

A survey from the American Bankers Association found that fewer non-qualified mortgages were originated in 2016 after regulatory requirements and other risks scared some banks out of the market entirely.

In fact, some 30% of banks surveyed said they stopped making non-QM loans for those reasons.

That pushed the non-QM share to around nine percent from 14% in 2015. When the loans were first introduced in 2014, they held a similar share.

It’s unclear what the non-QM market share will be in 2017, but if it’s up from last year, and expected to double or triple, it could be pretty significant in 2018.

In the 2016 survey, nearly half (44%) of respondents cited “loans exceeding the debt-to-income ratio” as the most common reason for not meeting QM standards.

Should Give Rise to a Healthy New Market

That brings up another point made by the S&P, and more specifically, global structured finance research senior director Tom Schopflocher.

He noted that non-QM loans tends to be absent risk layering, meaning they shouldn’t perform as poorly as subprime and Alt-A loans, those which they are often compared.

The problem with the mortgages seen a decade ago had a lot to do with layered risk, whereby applicants had low credit scores, no down payments, and very little verification of income and assets, if any.

It was essentially a triple whammy that gave the underlying loans no shot at survival, especially as home prices tanked.

While non-QM may not fit the Qualified Mortgage definition, they still have to satisfy the Ability-to-Repay rule. And this often means making loans to borrowers with a lot of assets, even if income is a bit more questionable or unsteady.

As more and more players enter the space, liquidity should improve, as should confidence to lend outside the QM box. We’re already starting to see residential mortgage-backed securities (RMBS) that contain non-QM loans hit the market.

That could result in a surge of applications and usher non-QM into the mainstream. At the moment, it’s not a household name, but it could well be if its market share rises to 20-30% of applications.

Let’s just hope it becomes popular for the right reasons and doesn’t earn the same reputation subprime did.

Subprime was fine until –along with the Alt-A market and even conforming stated, the LTV’s go wild.