A new survey from the Federal Reserve and the Conference of State Bank Supervisors (CSBS) revealed that the majority of community banks are already originating non-QM loans.

This is somewhat surprising, given they’ve only recently come into existence, along with the uncertainty regarding liability.

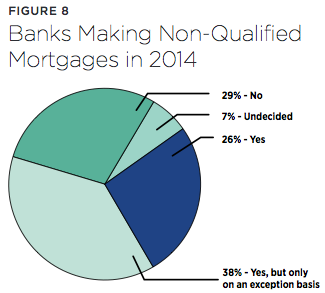

Still, 26% of survey respondents indicated that they were indeed making non-QM loans, while another 38% said yes, but only on an exception basis.

Only 29% of bankers said they weren’t offering such loans, which is lower than most would probably think for such a new, untested home loan product.

Another 7% said they were still undecided, which is no surprise since they’ve only been available since January.

It also seems as if certain banks are focusing more on non-QM loans than others.

For example, 15% of lenders said 80% or more of their mortgages would not meet QM requirements.

But for the large majority, only 0-10% of mortgages would fall outside of QM.

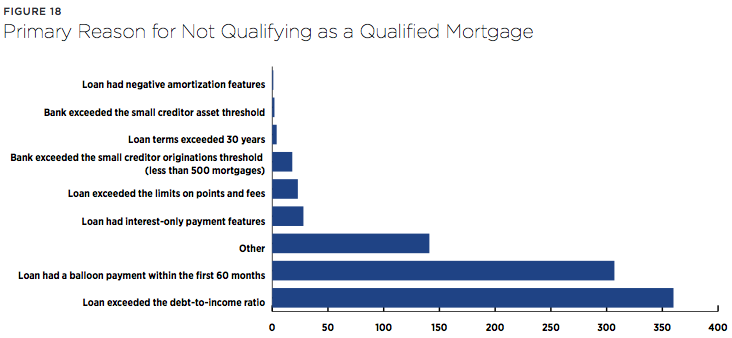

The primary reason for not qualifying under the QM rule was a loan that exceeded the DTI threshold of 43%.

It was followed by loans that have a balloon payment within the first 60 months.

Less frequent responses included loans with interest-only features and loans that exceeded the points and fees allowed for QM loans.

The survey also asked bankers if they were eligible to make rural, balloon-payment qualified mortgages.

Half of the respondents said they could, and of those, 65% indicated that they would offer such loans in 2014.

A recent survey from Fannie Mae revealed that 80% of lenders don’t plan to originate non-QM loans, or take a wait-and-see approach.

Check out the lenders actively participating in the non-QM market.